Control Your Financial Destiny with a Personal Tax Free Retirement Plan.

With a personal tax free retirement plan you are in control. You decide how much to contribute and when to take out your money. Not the Federal Government.

Retirement Strategies: Your Personal Tax Free Retirement Plan. Watch the Video it’s a game changer.

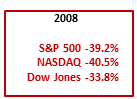

Your Personal Tax Free Retirement Plan is better than an IRA, 401(k) or 403(b) retirement plan. You don’t lose money when the markets go down. You share in market upside when the markets go up. You earn reasonable rates of return and gains are locked in. You can access your money tax-free and penalty free at any time for any reason.

You are in control. You choose how much to contribute (no limitations) and when to withdraw money (no RMDs).

Best kept secret to financial independence – Your tax-free pension alternative

Best kept secret to financial independence – Your tax-free pension alternative

The sooner you start the more powerful this strategy becomes. You can use this as a catch up solution if you have not put enough away for retirement. Qualified plans (IRAs, 401(k)s 403(b)s) have annual contribution limitations- see chart. There are no such limitations with the tax-free retirement plans. You can set up a plan where you contribute $100,000 a year for 3 to 5 years or longer.

Free retirement plan comparison

Free retirement plan comparison

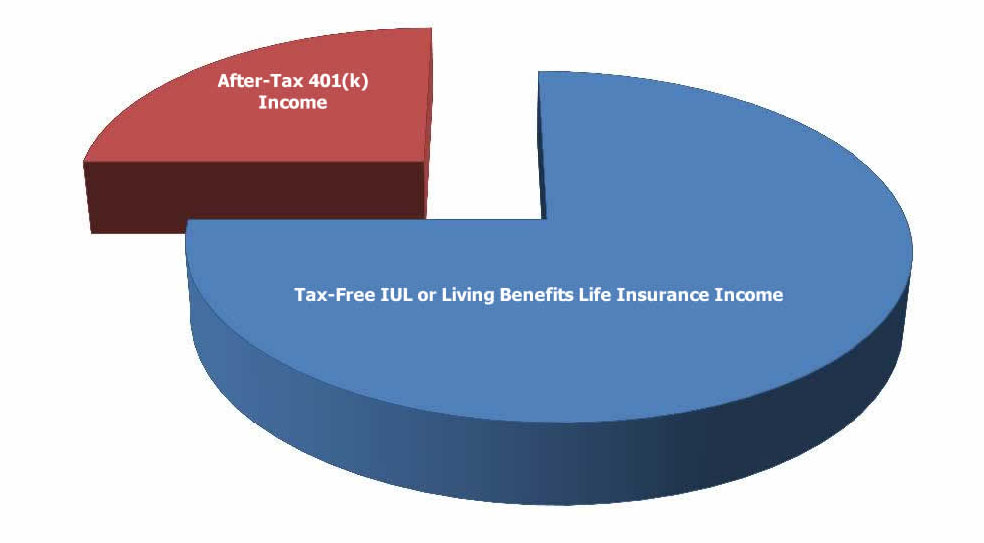

Retirement Plans are heavily taxed. Did you know that if you withdraw $50,000 from you 401(k), the IRS could take $20,000? Did you know if you leave $500,000 in your 401(k) to your spouse or kids, the IRS could take $200,000? The tax-free retirement plan is a little known IRS strategy that the wealthiest top 10% of American Families, including the top 1% have been using for more than 20 years to cut taxes and preserve capital.